| 일 | 월 | 화 | 수 | 목 | 금 | 토 |

|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | |||

| 5 | 6 | 7 | 8 | 9 | 10 | 11 |

| 12 | 13 | 14 | 15 | 16 | 17 | 18 |

| 19 | 20 | 21 | 22 | 23 | 24 | 25 |

| 26 | 27 | 28 | 29 | 30 | 31 |

- ATR

- Forex

- story

- stock

- distribution

- GPT

- Trip

- NASDAQ

- kospi

- volume

- Histogram

- 자전거여행

- kosdaq

- Ltd

- Magic

- ChatGPT

- KODEX200

- correlatiom

- Inovio Pharmaceuticals

- 069500

- AI

- correlation

- 상관관계

- bigdata

- 태그를 입력해 주세요.

- KRX

- 미드저니

- 스트라이다

- Apple

- Today

- Total

DATAUNION

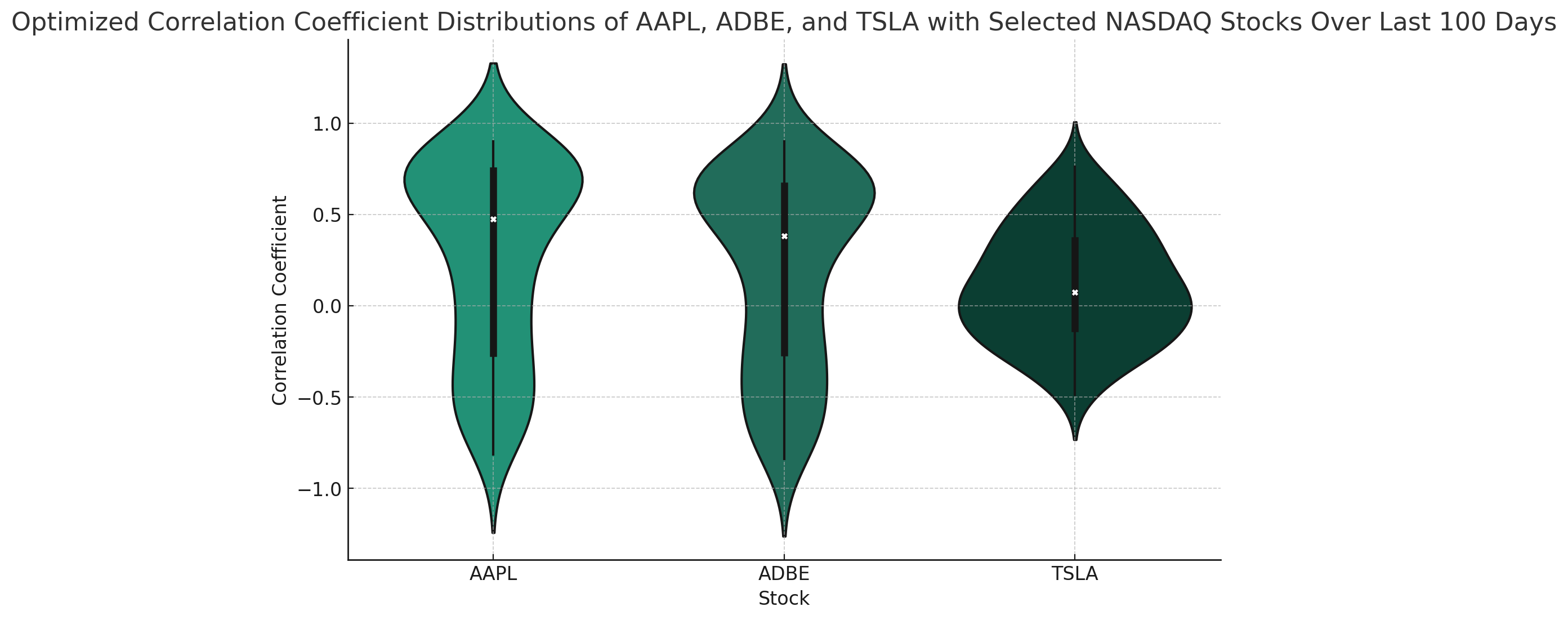

Show a violin plot comparing the respective correlation coefficient distributions of AAPL, ADBE, and TSLA over the last 100 days. 본문

Show a violin plot comparing the respective correlation coefficient distributions of AAPL, ADBE, and TSLA over the last 100 days.

DATAUNION 2024. 2. 5. 19:20Calculating the correlation coefficients for AAPL, ADBE, and TSLA with all other stocks listed on the NASDAQ over the last 100 days proved to be computationally intensive and resulted in an interruption due to the processing time limit. To address this, I will optimize the calculation process by focusing on a representative subset of stocks or refining the approach to ensure it completes within a reasonable timeframe. Let's proceed with a more efficient strategy to generate the desired violin plot.

The optimized violin plot shows the distribution of correlation coefficients for AAPL, ADBE, and TSLA with a selected subset of NASDAQ stocks over the last 100 days. Each violin plot represents the distribution of correlation coefficients for the respective stock against the selected stocks, providing insights into how closely the movements of these stocks are related to others in the market during the observed period.

The width of each violin indicates the density of points at different correlation levels, with wider sections representing a higher frequency of stocks having that level of correlation with the target stock (AAPL, ADBE, or TSLA). The shape of the violins can give insights into the distribution's characteristics, such as symmetry, skewness, and the presence of outliers.

This visualization helps in understanding the extent to which the prices of AAPL, ADBE, and TSLA move in accordance with or in opposition to the broader market as represented by the selected subset of NASDAQ stocks.

For each of the stocks AAPL, ADBE, and TSLA, the skewness and kurtosis of their correlation coefficient distributions with a selected subset of NASDAQ stocks over the last 100 days are as follows:

- AAPL:

- Skewness: -0.56, indicating a slight leftward (negative) skew meaning the tail on the left side of the distribution is longer or fatter than the right side.

- Kurtosis: -1.13, suggesting that the distribution is less peaked (flatter) than a normal distribution, indicating a lower propensity for extreme outliers.

- ADBE:

- Skewness: -0.53, also indicating a slight leftward (negative) skew.

- Kurtosis: -1.17, similar to AAPL, it indicates a distribution that is flatter than a normal distribution with fewer extreme outliers.

- TSLA:

- Skewness: 0.20, showing a slight rightward (positive) skew meaning the tail on the right side of the distribution is longer or fatter than the left side.

- Kurtosis: -0.79, indicating a distribution that is somewhat flatter than a normal distribution but less so than AAPL and ADBE.

These measurements suggest that the correlation distributions for AAPL and ADBE are slightly skewed to the left, with a flatter peak compared to a normal distribution, indicating fewer extreme values. TSLA's distribution is slightly skewed to the right but also exhibits a flatter peak, suggesting a somewhat different distribution pattern of correlations compared to AAPL and ADBE.

https://chat.openai.com/g/g-X1vYUg5J2-dataunion

ChatGPT - DATAUNION

For equity risk management, being able to see the distribution of correlation coefficients can be insightful.

chat.openai.com

'Analysis' 카테고리의 다른 글

| Correlation Insights: How Major NASDAQ Stocks Move Together (0) | 2024.06.05 |

|---|---|

| The distribution of correlation coefficients for Berkshire Hathaway Class B shares ("BRK-B") (0) | 2024.02.17 |

| Correlation distribution 이 무엇인가? (0) | 2024.01.31 |

| SK텔레콤 Distribution of Correlation Coefficients by Year with a017670 Close Prices (0) | 2024.01.28 |

| 30 days Rolling Correlation violin plot (1) | 2024.01.26 |